Land Tax is a wealth tax payable by landowners in Australia, annually, on the value of their land.

It is one of three forms of taxation payable by real estate owners in Australia. The other two forms are Transfer Duty (also known as Stamp Duty) payable on the purchase of real estate and Capital Gains Tax payable on the sale of real estate.

This article explains Land Tax in Australia.

How does Land Tax work?

Land Tax is a State Tax, which means that each State and Territory in Australia has their own laws for the tax, and most importantly, the land value thresholds and rates of tax payable.

The Land Tax Laws of the Australian States and Territories contain these features:

- Each State and Territory imposes land tax independently of the other.

- Land tax is payable by the owner on the taxable value of all land they own in the State. This means that land held outside of the State is not included in the land tax assessment.

- Land tax is payable if the taxable value of the land is above the tax threshold. The rate increases according to land value. A table of thresholds and rates is set out below.

- Some land is exempt from land tax. Land is exempt if it is used as a principal place of residence, or for primary production or for a charitable purpose such as education, hospital, aged care, and low-cost accommodation.

- The taxable value of land is the unimproved value / site value of the land. The phrases unimproved value / site value mean the land value without regard to improvements made on the land.

- In some States, taxable value of land is the latest land valuation. In other States, the taxable value is the average of the current and select past year land valuations.

- Land tax is charged annually on land owned at a defined time and date. The taxing date is midnight on 31 December (NSW, Vic) or on 30 June (Qld, WA, SA, Tas), and applies to the following year, or in the ACT, to the following quarters.

- Foreign persons / absentee owners must pay Surcharge Land Tax in addition to land tax payable if the land is residential land. This includes homes (principal places of residence) which would otherwise be exempt from land tax.

- The Surcharge Land Tax rate varies between 0.75% and 4% per year, depending on the State. See the table below.

- Surcharge Land Tax is payable in all States except in Queensland where surcharge land tax is payable on all land, and in South Australia and Western Australia where no surcharge land tax is levied at all.

- Land tax is levied according to ownership. This means if an owner owns more than one parcel of real estate, the values of the multiple properties are aggregated (added together) for land tax purposes. Ownership can be direct, or through a trust.

- In most States, if land is owned by related companies, the companies are grouped, and their land holdings are aggregated to determine the amount of land tax payable.

- Land tax can be passed on to tenants under some leases as an outgoing. This applies to commercial leases. Land Tax cannot be passed on under residential and retail leases.

- The conveyancing practice is that all land tax is cleared when title is transferred because if it is not, the purchaser becomes liable to pay the land tax payable by the seller of the property.

How is land tax calculated?

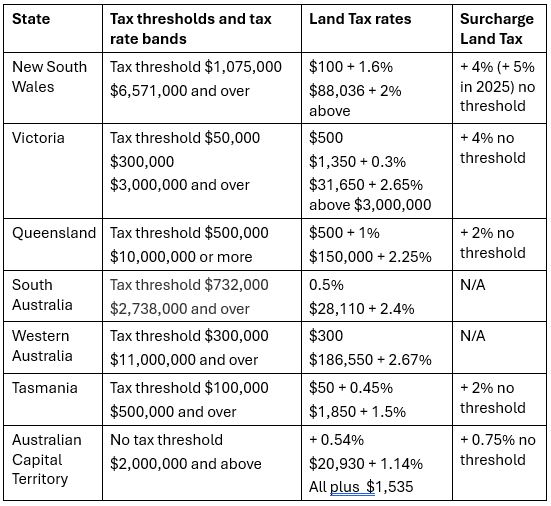

This table contains a general summary of land tax thresholds, land tax rates and surcharge land tax rates in each State and Territory in Australia (current 2024/2025).

On what property is land tax paid?

Land Tax is levied on a wide range of properties –

- vacant land, including rural land

- land where a house, residential unit or flat has been built

- a holiday home

- an investment property or properties

- company title units

- residential, commercial or industrial units, including car spaces

- commercial properties, including factories, shops and warehouses

- land leased from state or local government.

Rules for land valuations

Land is valued by the Valuer General at market value to determine the unimproved land value / site value of the land for land tax purposes.

Land value does not include the value of buildings or structural improvements or the legal effect of restrictions such as easements. But it includes works such as draining, excavating, filling, clearing and retaining walls. For consistency, land values reflect the property market as at the taxing date in the valuing year.

As a rule of thumb, the ratio between land value and market value for an apartment is in the range 10% - 30%, and for a house is in the range 40% - 60%. So, if an apartment is valued at $900,000, the land value component is between $90,000 and $270,000 – which is the land value upon which land tax is levied.

Other land taxes

In some States and Territories, other taxes are added to land tax assessments. In Western Australia, a Metropolitan Improvement Tax of 1.4% is added. In Victoria, a Vacant Residential Land Tax (known as a ghost tax) is imposed at 1% (increasing to 2% in year 2, then 3% in year 3) of a vacant property’s capital improved value. This tax applies to Australian resident owners of holiday houses unless occupied by owners or their relatives for at least four weeks a year.

Land tax for trusts

In some States and Territories, higher land tax rates are payable for land held in a trust. In others, there may be a lower, or no, tax threshold. In NSW no tax threshold applies to land held in a special trust, which means a discretionary (i.e. family) trust. In Victoria, land held in a fixed, discretionary or unit trust is generally assessed at trust surcharge rates. In Queensland and in South Australia a lower land tax threshold applies to land held in a trust.