Landlords of strata properties face an added layer of complexity when claiming strata levies as tax deductions.

The added layer of complexity is that some strata levies are rental expenses that can be claimed now while other strata levies are claimed over several years.

The Australian Taxation Office (ATO) in the Rental Properties Guide tells how different strata levies are to be treated as rental expenses.

This article aims to help landlords of strata investment properties to apply the ATO’s guidance. But first, it is necessary to find out more about strata levies.

All about strata levies

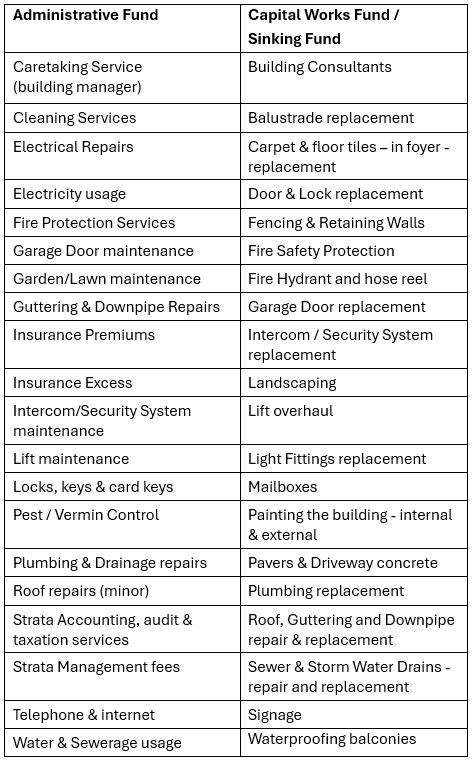

Some strata levies are paid into the Administrative Fund, others are paid into the Capital Works Fund (also known as the Sinking Fund).

The difference between the funds is that the Administrative Fund is used to pay for day-to-day expenses, while the Capital Works Fund / Sinking Fund is used to pay for capital works expenditure.

These are lists of allowable payments from each Fund.

Notes

- Strata law requires owners corporations / body corporates to maintain two separate funds, the Administrative Fund and the Capital Works Fund / Sinking Fund. [note: the terminology differs between the Australian State Strata Laws]

- The Administrative Fund is used to pay for day-to-day expenses such as administration, maintenance and repair of the common property, recurring expenses, and insurance. The levies for the Administrative Fund are budgeted annually based on existing and estimated items of expenditure, at the Annual General Meeting. Owners pay levy contributions quarterly.

- The Capital Works Fund is used to pay for major work, often replacement of the external and internal items of the building and the common property. The levies for the Capital Works Fund are budgeted on estimates for significant capital items or major works planned to be done over a period of several years [10 years is the mandatory plan period in NSW]. The works scheduling is decided by the owners corporation / body corporate at the Annual General Meeting. Owners pay levy contributions quarterly.

- Strata law permits the owners corporation / body corporate to raise Special Levies / Special Purpose Levies when there are insufficient funds in the Capital Works Fund to pay the cost of major work which cannot be deferred, or which is unforeseen work. Often, Special Levies are large, and can be made payable by instalments.

Examples of major work for which Special Levies are raised are:

- Balcony rectification (treating concrete cancer, waterproofing, new balustrades)

- Building Defects claim for new buildings – to fund recovery action

- Removal of combustible cladding

- Complete replacement of windows and external doors

- Lift refurbishment and replacement

- Severe damage to roof and building caused by fire or storm and tempest, flood

How does the ATO treat strata levies as landlord rental expenses?

The ATO Rental Properties Guide contains a Rental Expenses webpage which deals with strata levies.

This is the link Body corporate fees and charges.

This is an extract:

Regular payments you make to body corporate administration funds or general purpose sinking funds for ongoing administration and general maintenance are considered to be payments for the provision of services by the body corporate. You can claim a deduction for these regular payments at the time you incur them.

However, if you are required by the body corporate to pay a special levy to fund a particular capital improvement, these levies are not deductible. This is the case whether that special levy is paid into a special purpose fund or as a special contribution to the general purpose sinking fund.

If the body corporate does raise a special levy to fund certain types of construction costs, you may be able to claim a capital works deduction. You can only claim a capital works deduction once the work is completed and the cost has been charged to either:

-

- the special purpose fund, or

- the general purpose sinking fund, if a special contribution has been levied.

If the body corporate fees and charges you incur are for things like:

-

- the maintenance of common gardens

- deductible repairs and building insurance

you cannot also claim a deduction for similar expenses. For example, you cannot claim a separate deduction for common garden maintenance if that expense is already included in body corporate fees and charges.

The ATO also has an Apartment building defect expenses webpage, which details the ATO’s position on tax deductions for combustible cladding.

This is the link Combustible cladding replacements you can claim.

This is an extract:

You can claim a deduction for costs you incur to replace or contribute to the replacement of combustible cladding to meet government requirements.

To be able to claim a deduction, you must replace the combustible cladding with fire resistant cladding. You treat the replacement of the cladding as capital works. This is because we treat the replacement of cladding as:

-

- an entire functional structure (being the outer covering of the building)

- an improvement in the function of the outer covering of the building.

This means the building is no longer a fire hazard and becomes fire resistant as an improved functional operation of the cladding.

You can claim a deduction for the amount you contribute over a period of either 25 or 40 years. That is, 4% or 2.5% of the cost of the improvement being allowed in each year.

The replacement of combustible cladding doesn't meet the requirements to be deductible as a repair or environmental protection activity.

Comment – Why wise strata investors love capital works/sinking fund levies (and hate special levies)

The wise strata investor loves Capital Works / Sinking Fund.

This is because the Capital Works / Sinking Fund is a general purpose fund, which means that levies paid into the Fund are used to pay a wide variety of building improvements and refurbishment such as painting, a new roof, new carpet, new driveway or lift overhaul, as well as repairs.

Normally, these improvements and refurbishments would be treated as capital work expenses to be deducted over several years.

But because the Capital Works Fund / Sinking Fund is a general purpose fund, the ATO allows the investor to claim the levies paid into the Fund as rental expenses in full in the year of payment.

Contrast and compare Special Levies / Special Purpose Levies, which are levies raised to fund a particular capital improvement or capital work. The ATO requires the investor to claim the levies as a capital works deduction which is spread over a period of either 25 or 40 years.

For more information about tax deductions for landlords, click on this link to my article and video Tax deductions for landlords - the ATO Rental Properties Guide

Roof Repairs to a Strata Apartment Complex – for an investor, if the roof repairs are paid from the Capital Works / Sinking Fund, then the investor can claim the levies paid into the Fund as rental expenses in full in the year of payment. But if the roof repairs are paid from a Special Levy, then the levy can only be claimed as a capital works deduction over up to 40 years.

Roof Repairs to a Strata Apartment Complex – for an investor, if the roof repairs are paid from the Capital Works / Sinking Fund, then the investor can claim the levies paid into the Fund as rental expenses in full in the year of payment. But if the roof repairs are paid from a Special Levy, then the levy can only be claimed as a capital works deduction over up to 40 years.