Ending a telephone call with the words: “You’ve got nothing in writing … Good luck if you want to try and get anything in court” is an excellent way to provoke a lawsuit. Particularly if the call was made by a joint venture partner to request payment of a profit share in a successful property venture.

In this article, we analyse how it was that two property developers, John Cappello and John Scrivener, litigated over a profit share of over $9 million in a property venture because they did not put their property joint venture into writing.

The case study is the decision Cappello & Anor v Scrivener & Anor [2020] NSWSC 1748 (7 December 2020) (Stevenson J).

We conclude with an analysis of what could have been done differently.

Outline of events

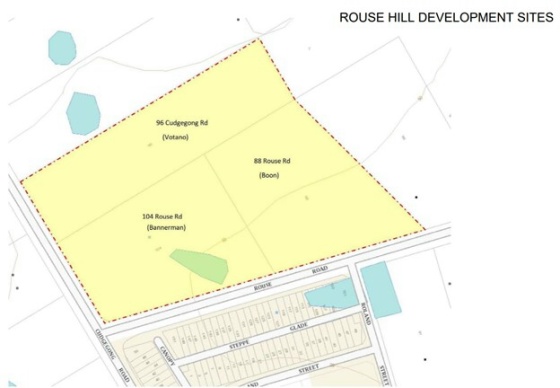

From February 2013, Mr Cappello, a local real estate was trying to consolidate three adjoining 5 acre properties at Rouse Hill in Sydney as a site for medium density & small lot housing. He made his offers through a local real estate agent. By August, two of the property owners had accepted his offers.

He contacted Mr Scrivener, a property developer from the Gold Coast in Queensland. On 20 August 2013 they met and reached a verbal agreement to:

- endeavour to secure the three Rouse Hill sites (see image at the end of the article);

- sell the combined site at a profit;

- pay equally “expenses” or “costs”; and

- share equally any profit.

Mr Scrivener looked after all the negotiations and legal documentation because Mr Cappello was a local real estate agent and wanted to remain a silent partner. Due Diligence Deeds, and subsequently the Put and Call Options were entered into by Mr Scrivener’s companies.

In November 2013, they reached agreement with the third property owner. Mr Scrivener was so pleased that he made a diary note: “The fish and chips are on the stove – now got 17 months to make sure I make it all happen.”

The joint venture partners had secured the three sites for a total price of $12.734 million.

In December 2013, the due diligence period was due to expire for one property. A Put and Call Option was granted to Mr Scrivener’s company Tuscany. Mr Cappello and Mr Scrivener each contributed one half of the option fee paid of $250,000 and the legal fees. At this time, Mr Cappello asked that the joint venture be recorded in writing. It never was.

A key dispute was Mr Scrivener’s assertion that the joint venture agreement contained a Sunset Date. He said that Mr Cappello had told him on 20 August 2013 that “We can flick [the options] on before the due diligence period is up”, that is, by 28 February 2014 (the “Sunset Date”).

Mr Cappello tried, but did not achieve a sale by the Sunset Date at a price of $16.5 million. In the meantime, the due diligence periods for the other two properties were about to expire.

On 14 March, 2014, Put and Call Options were entered into for the other two properties by Mr Scrivener’s companies. The joint venture partners did not contribute to the option fees. Mr Scrivener had arranged funding for the option fees from Oracle Estates, a property development group, under a loan agreement.

A Property Development Feasibility Study was prepared. In May 2014, Mr Cappello tried again, but was unable to sell, the site.

On 6 August 2014, Mr Scrivener’s companies entered into a Development Management Agreement with Oracle Estates to obtain development approval for the subdivision and sale of the properties. Oracle Estates agreed to fund all development expenses and the purchase price of the properties. They agreed on a profit share.

Oracle Estates paid a 2% acquisition fee of $280,060 to Tuscany, of which Mr Cappello received one half. In addition, Oracle Estates reimbursed the option fee paid of $250,000, of which Mr Cappello received one half.

In May 2015, Blacktown City Council granted approval to develop the site for a medium density subdivision. The options were exercised by Tuscany/Oracle Estates.

On or about 20 July 2015, the site was sold for $37 million. The profits were split 45.52% to Tuscany and 54.48% to Oracle. Tuscany received $9,141,937.95 as its profit share under the Development Management Agreement.

Mr Scrivener refused to recognise that Mr Cappello was entitled to share in this profit. Mr Scrivener relied on what he had said in December 2013 that: “this journey for you is over if the site is not sold before the DD period expires”. That is, the joint venture no longer subsisted because Mr Cappello had not sold the options by the Sunset Date.

The findings and proposed orders

The Court made these findings and orders:

- “it was Mr Cappello who introduced Mr Scrivener to the project and thus make available to Mr Scrivener [and his company] Tuscany the opportunity from which they have now profited.” [at 436]

- “in December 2013, Mr Cappello asked that the arrangement between them be documented, the result of which would have been that Mr Cappello, or his wife, would also have been “on the hook” financially.” [at 437]

- “consistently between 20 August 2013 and the Sunset Date, Mr Scrivener referred to Mr Cappello as his joint venturer or joint venture partner.” [at 450]

- “Mr Cappello’s involvement after the Sunset Date, is inconsistent with Mr Cappello being, at that stage, a mere investor. Mr Cappello’s involvement appears to be that which would ordinarily be expected of a motivated joint venture partner.” [at 332]

- “As I am persuaded that the [Sunset Date] was not a part of the 20 August 2013 agreement, and as I find there was no breach by Mr Cappello of the [financial contributions] condition, I find that there was a partnership between Mr Cappello and Mr Scrivener of the kind for which Mr Cappello contends.” [at 465]

- “I propose to make a declaration to the effect of that sought by Mr Cappello, namely, that there was a partnership between themselves and/or their corporate nominees (Tuscany in the case of Mr Scrivener and a company later to be nominated by Mr Cappello) which acquired the rights to control and sell the three contiguous properties situated at 88 Rouse Road, 104 Rouse Road, and 96 Cudgegong Road, Rouse Hill.” [at 467]

- “Mr Cappello [has] elected to receive equitable compensation.” [at 470]

Analysis: What could have been done differently?

The Court decided to enforce the verbal joint venture agreement as a partnership agreement. This was in order because partnership agreements do not need to be in writing.

What could have been done differently? We start with the obvious – that the agreement made on 20 August 2013 needed to be in writing. An email exchange would have been sufficient, although a Heads of Agreement or formal Joint Venture Agreement (JVA) signed by the partners would have been better. In this case, not even a note was made.

Mr Cappello should have presented a formal JVA in December 2013, before he contributed $125,000 for the option fee for the grant of an option to Mr Scrivener’s company (Tuscany) of which he was neither a director nor shareholder.

The JVA would have needed to be varied later. As the Court said:

“As things turned out, the project evolved into one far more ambitious than that contemplated on 20 August 2013. Mr Scrivener procured the active and substantial involvement of Oracle. The Put and Call Options were entered, and the vehicle for the Tuscany/Oracle joint venture exercised the call options and acquired the sites. Development Approval was obtained, and the combined site sold to Tian Tong to the significant profit of Oracle and Tuscany.” [at 440]

One variation to the JVA could have been to compensate Mr Scrivener for his substantial contribution of time and effort to involve Oracle Estates as a funder and then as a joint venture partner and to pursue the development approval. The “exposure” of Mr Scrivener and his companies to the potential liability of being legally bound to purchase the properties for the total price of $12.65 million should also have been compensated. The form of compensation would normally be a greater profit share.

The Court order reflects this. The Court awarded “equitable compensation” to Mr Cappello, not 50% of the profit, so as to compensate Mr Scrivener for his time and effort and his liability exposure.

An alternative would have been an incorporated joint venture. That is, a joint venture company as the vehicle is used to conduct the joint venture. Mr Scrivener could have been the sole director and secretary, with Mr Scrivener’s and Mr Cappello’s own companies as equal shareholders. The Court highlighted Mr Cappello’s weak position as a silent partner by not having a joint venture company to protect his interests:

[Mr Cappello’s counsel was correct to submit that] “This was not a case where the parties chose to conduct their business through a corporate vehicle. Mr Cappello was not a director or shareholder of Tuscany and there was never any suggestion he would be. Mr Scrivener had sole control of Tuscany and the commercial opportunities which arose from the agreement of the parties that the partnership be conducted on the basis that Tuscany held the partnership assets and Tuscany be the party entering into relevant due diligence deeds, option deeds and project management agreements.” [at 466]

While an incorporated joint venture provides a good framework, it is always best to have a joint venture agreement between the shareholders to document the terms of the joint venture.

Source: Annexure A to the judgment